This repository contains utilities that will help you maximize your wealth and pay less in taxes. The core component is a financial simulator that simulates every year of your life. It will contribute to accounts in the most tax-efficient order. And during retirement, it will withdrawal from the most tax-efficient accounts.

- python (3.8+)

- matplotlib

- rich

Not trying to hide this stuff, but here are some gotchas. Most of this stuff boils down to it being very difficult to predict the future. But some things were intential design decisions.

- There are no gaps in employment.

- Pay raises are constant (unrealistic, I'm aware).

- Any excess income will go into a taxable account.

- After retirement and before RMDs, you will do Roth IRA conversions. This amount is automatically calculated to produce the highest assets at death. Note: this currently assumes your marital status does not change during this post-retirement/pre-RMDs period. I understand that this will not work for everyone.

- During RMDs, you will withdrawal at least your standard deduction. This is amount is taxed at 0%.

- Excess RMDs are transferred to a taxable account, where it grows at the same interest rate as retirement accounts.

- Standard duduction only.

- Only "single" and "married" filing statuses.

- If there are traditional investments at death, it assumes that one of your children will inherit the remainder. Your child will be 30 years younger than your age of death. They will be expected to take RMDs based on the IRS Single Life Expectancy table. The taxes they expect to pay for this will be included in your total taxes. Assuming your child has no income for the remainder of their life, this will be the minimum expected tax.

- Outside of estate taxes, there are no taxes for taxable and Roth investments at death. For taxable accounts, the step up in basis plays a significant role in helping to reduce taxes after death.

- Interest is applied at the end of each year.

- The "market" has no volatility. Investments grow at a steady rate.

- Divorce is not possible. Once you are married, you are stuck that way.

- Spending remains constant thoughout your lifetime. Once again, this is unrealistic but necessary. Because interest rates are real, this number accounts for inflation.

Given all of the initial variables (parameters), this script will simulate your portfolio and show you each year of your life. Running the following command will produce the graph below:

./source/sim.py

A simulation with more options, like this:

./source/sim.py \

--current-age=25 \

--income=100000 \

--starting-balance-trad-401k=100000 \

--max-contribution-percentage-401k=0.50 \

--employer-match-401k=0.07 \

--employer-contribution-hsa=750 \

--do-mega-backdoor-roth

Will look like this:

The graph.py utility is meant to help you determine how long to wait before

starting to defer taxes via pre-tax contributions, rather make than Roth

contributions. The lines represent your total assets (estate) after taxes at

death. The goal is to maximize this value. The higher (vertically) the line the

better. It should be noted that lines (interest rates) are independent from one

another. The total assets will be vary widely between different interest rates.

The lines are normalized to fit between 0.0 and 1.0 so they can be easily

compared.

./source/graph.py

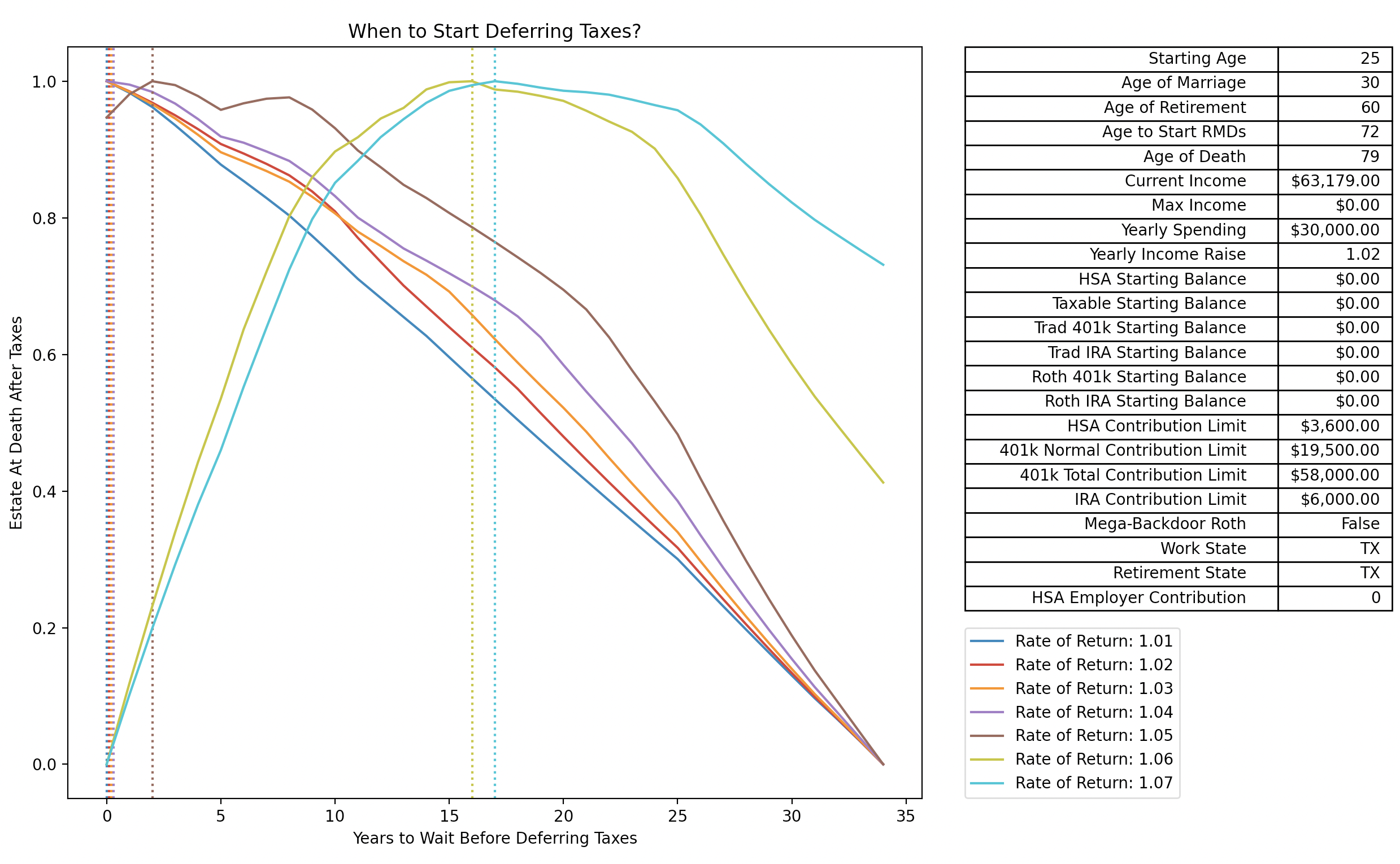

The figure below shows the typical American. They make a little more than $60k/year. Unlike the typical American though, they max out their retirement accounts each year. This figure shows that if you expect the long-term real interest rate to be 6% or higher, you might be better off making Roth contributions for a few years.

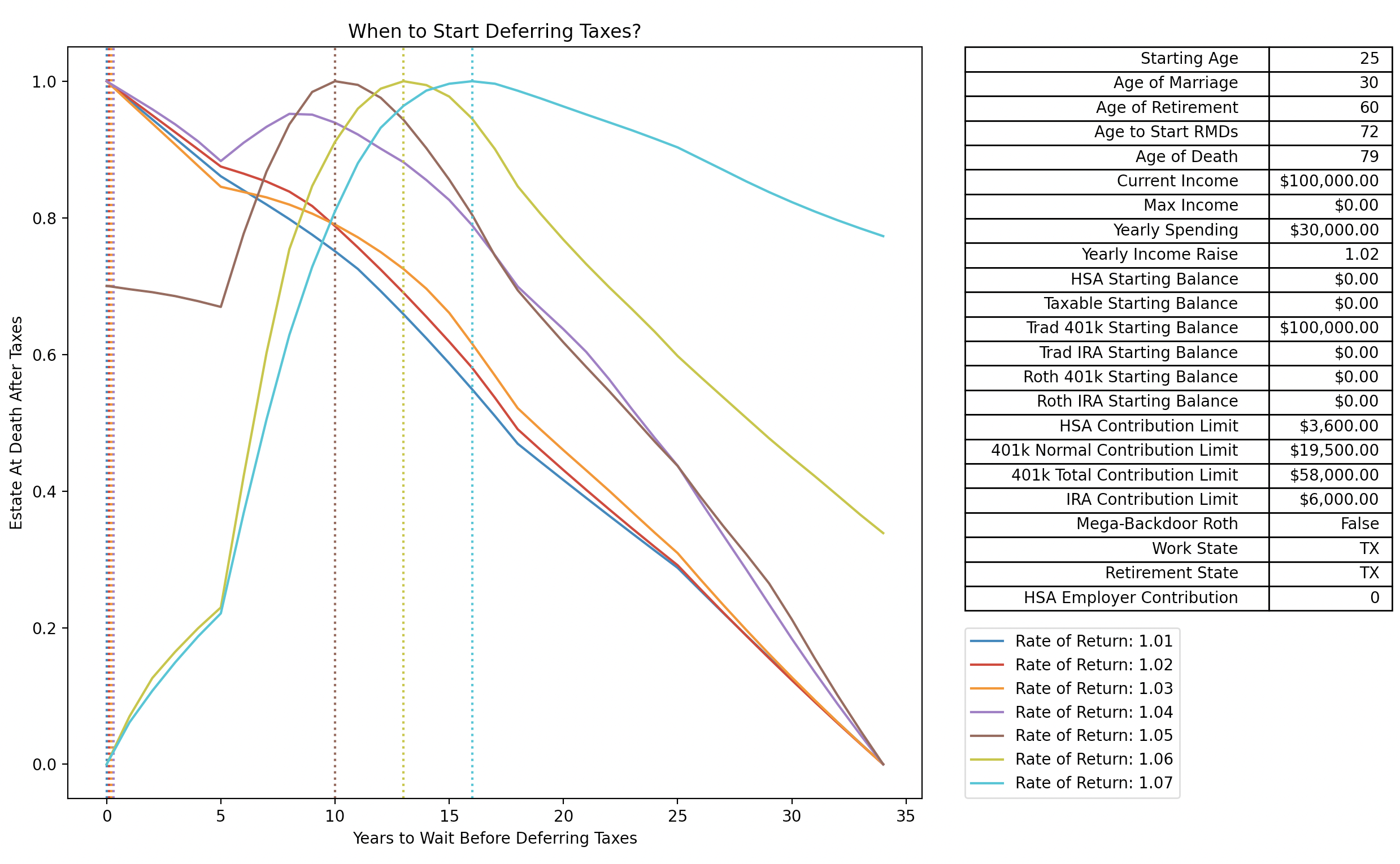

Though, if the same person in the figure above were to have $100k already saved in their traditional retirement accounts, the outcome would be quite different. The (relatively) small amount grows exponentially and requires higher RMDs.

Next, we have a slightly younger person, 25, that is just starting their career. They have nothing in their retirement, but they graduated without debt and got a decent job out of college making approximately $63k/year (what the typical American makes). With long-term interest rates of 5%, 6%, and 7% this person should prefer Roth contributions for at least the first decade of their career. Note: for all of the figures with a starting age of 25, the little upticks at year 5 are a result of becoming married. Due to better tax rates, you will pay less in taxes and invest more.

Say the same recent graduate got a job making $100k/year instead of $63k/year. What would change? Well, because of their higher income, traditional IRA contributions are not deductible. There is no point in contributing to a non-deductible IRA. Instead, they would contribute to a Roth IRA. For this reason, it appears that this person would get less out of Roth contributions than the previous lad.

Next, let's say the person above has a coworker that is the same age and has the same income, but spends twice as much (from $30k to $60k). What would change? Well, not much honestly. Their tax-advantaged savings should be on par, just their taxable savings would be different.

Next, assume one of these lads were real lucky and got an internship at a nice company during college, and somehow they found a way to sock away $100k into their traditional retirement accounts. This definitely pushes the scale towards Roth contributions for the beginning of their career.

Let's jump back to the new-grad making $63k/year, but say this person really wants to retire early, say at 50 years old instead of 60. Unless their investments can provide a 7% real return, they will probably be better off purely contributing to traditional retirement accounts.

On the other hand, what happens if this person decides to work a little bit longer, till the age of 70. Will this change things? By golly, it will. Unless their investments do very poorly over a long time, this person will be better off starting with Roth contributions.

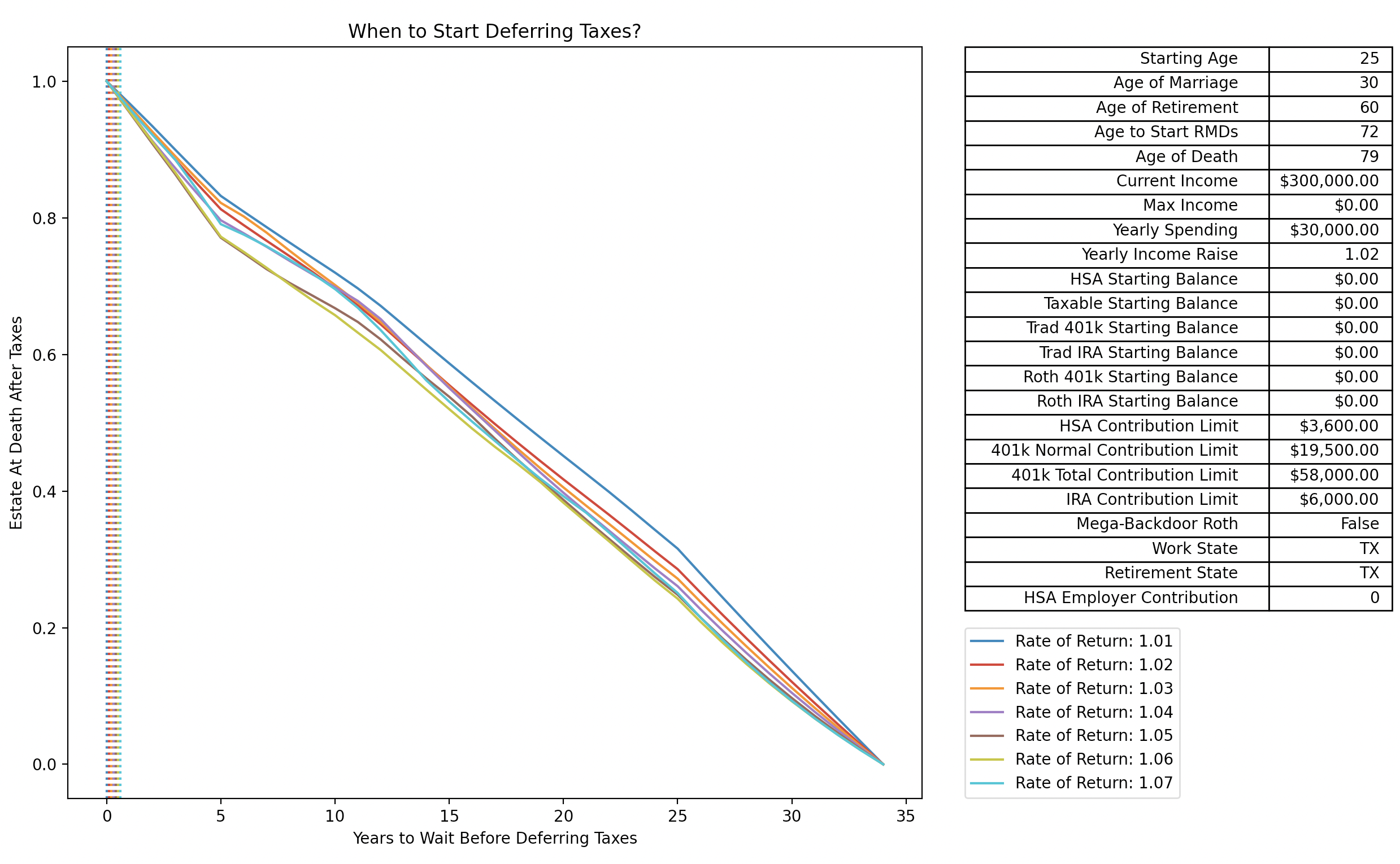

Next, let's say there's a hot-shot kid in Silicon Valley making $300/year and they want to retire at 40. Because they will have so few years in the workforce, traditional contributions will not make much of a difference in terms of RMDs. And because of their very high income, tax deductions are very valuable. These deductions do more good than RMDs do bad.

Let's say the same hot-shot kid decides he likes his job and wants to work another twenty years. The outcome is still the same. This person should always defer taxes. Their tax-rate is too high not to.

What if there is a kid who's income explodes (from $63k to $300k at a rate of 20% increases each year) while they are young? This person would reach an income of $300k at the age of 34, then plateau. This person should immediately start deferring taxes.